Broadridge’s LTX bond trading platform faces uphill battle

Entering a saturated market of electronic trading technology this summer, the new AI-powered platform must clear several hurdles before it can declare success.

A new corporate bond trading platform backed by Broadridge, dubbed LTX, is gearing up for an official launch in June, marking the three-year point since the project’s inception. During Broadridge’s fiscal year Q2 2021 earnings call on February 2, chief executive Tim Gokey said that the platform was “live in a soft launch with select clients”, and the firm was receiving “positive feedback.”

Gokey said this summer’s full launch will include “more than 10 dealers and 35 buy-side clients.” LTX chief executive Jim Toffey tells WatersTechnology that as many as 40 customers are already onboarded to the service, with another 80 in the pipeline ahead of the official roll-out.

LTX hopes it can offer an innovative trading solution that speeds up fixed income’s arduous, decades-long digital makeover. But others in the industry are skeptical of the upcoming release and say it is entering a saturated market for electronic bond trading platforms, one that perhaps not even Toffey, co-founder and former head of fixed income giant Tradeweb, can conquer.

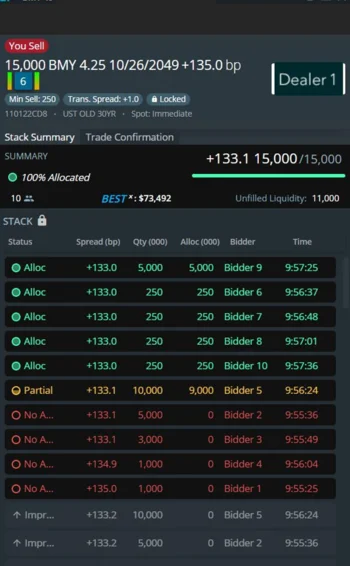

LTX’s central premise is that broker-dealers stand to gain better execution and price improvement by aggregating liquidity across multiple buyers. It offers an AI-powered trading platform that targets “natural” buyers and sellers for each security and gives respondents the opportunity to bid or offer their desired amounts through its proprietary, patented trading protocol, RFX, as an alternative to the widely used request-for-quote (RFQ) protocol.

Toffey says that back when Tradeweb began using RFQ for the first time, the idea was to take the way Treasury bonds were traded then—over the telephone—and make it electronic. “It wasn’t about creating a marketplace. It wasn’t about aggregating liquidity. There were a lot of things that I wasn’t trying to do. I was just trying to … electronify a phone call. And because of that, there are a lot of shortcomings in the way RFQ works today,” he says.

For example, if a customer wants to sell 10 million bonds, but the dealer only wants to buy 5 million, that’s not an option. With RFQ, buyers have to buy what the seller is selling, Toffey says. And while RFQs were a significant improvement on simple phone calls, they carried over one of the phone’s frustrations—would-be buyers could only guess what other buyers would bid for the same securities, allowing for little to no price improvement.

To remedy this, LTX will begin showing trade participants all the customers—identified not by name, but by bid amounts—that a dealer invites to a trade, allowing those participants to assess the pricing, liquidity, and interest of a bond in real time.

However, one senior executive in the voice trading space who is familiar with LTX doubts there is room for it in the market: “What you’re seeing is basically that MarketAxess, Tradeweb, Bloomberg, and now, I would argue, Trumid are the four electronic trading brands that people care about. Everything else is going to get sold for parts. And you’re seeing that all over the place, it’s not just credit. You don’t need 40,000 flavors of vanilla.”

The executive adds that the majority of notional volume is still traded using voice, years after fintechs began seeking to replace it, and says perhaps that’s solely because traders prefer it that way.

“So, if LTX is solving a problem that doesn’t really exist, it’s providing a solution that nobody’s asking for,” the executive says. But he acknowledges that he could be wrong about LTX’s prospects: “That being said, nobody knew they’d need Google Search. Nobody knew they needed an iPhone.”

Much like Trumid, founded in 2014, and its fast and somewhat surprising rise to rank among the industry’s stalwarts, LTX could flourish. Trumid’s secret ingredients, in the executive’s view, are threefold: a strong management team, good technology, and connectivity to the marketplace.

Kevin McPartland, head of market structure and technology research at consultancy Greenwich Associates, says LTX has some unique ideas that are made even more interesting by its access to Broadridge’s fixed income data.

The “natural” counterparties that LTX seeks out to complete trades are targeted using Broadridge’s years-long stockpile of banks’ post-trade fixed income data, which comprises records of many of the largest banks’ daily trades with each of their customers. Toffey says LTX would only access this data with a respective broker’s permission, but, if given, this dataset could provide brokers with the key to knowing exactly who they should put a trade in front of.

McPartland, who notes that the adoption of emerging technologies has been slow in fixed income, believes that what has been adopted has improved not only trading processes, but also market transparency and liquidity overall. He says LTX may prove to be another example of this.

“I would say that the evolution has been slow because old habits die hard, not because the old ways were better,” he says. “The old ways might have helped some people and some firms make more money, but in terms of execution quality and liquidity, it is quite hard to debate that the current market isn’t considerably better than it once was.”

A second fixed income specialist who offers consulting services believes that a platform like LTX is great in theory, with the caveat that what’s great in theory doesn’t always translate into what gets used and liked. Traders, especially in the insular fixed income community, are creatures of habit, and LTX—and other platforms that purport to upend well-established workflows—are likely to encounter some level of resistance.

“The tech and all the tentacles and the connections, and all the inner workings will probably be rock solid,” the specialist says. “But even when you have great tech, you might not implement it correctly, and then you’ll have some problems. So could LTX face some problems? Yes, but the bones of it are good—the tech of it is good. But I think Jim is going to have a hard time. And this is what happened with Benchmark.”

In 2009, shortly after leaving Tradeweb, Toffey had founded a new company called Benchmark Solutions, a bond pricing data provider. After four years, the business closed down after losing its backing from private equity firm Warburg Pincus. Its technology has since found a home at Bloomberg.

A former employee of Benchmark Solutions said one of its downfalls was a lack of consistent, aggressive client outreach, which they view as necessary for getting a new company off the ground.

Toffey says it’s true the company struggled to gain customers, but that was because the business was too narrow as a service offering. He adds that LTX potentially has a game-changer this time around in the form of its Broadridge-derived dataset.

“When a dealer says I want to use LTX to help my business grow, they sign one piece of paper, and we unlock all the data that dealer’s bought and sold with every single customer—thousands of customers over the last X years—to create the analytics. There is no other vendor on the planet that has access to that data but us,” Toffey says. Again, though, the broker would have to sign off on LTX using Broadridge’s data.

While Toffey and the rest of the team at LTX have been building out the product’s network effect prior to its official launch, he volunteers that a metric for gauging success will be whether at least 100 buy-side and sell-side shops are actively using the platform by the end of 2021. In terms of volume, the company is targeting 1-2% in market share, also by the end of the year.

Fully acknowledging that there’s a raft of rival offerings already out there, Toffey says he’s less concerned with competing with the likes of Tradeweb, MarketAxess, and Bloomberg, and much more keen to solve what he views as an elusive fixed income riddle: how to electronify the 70% of the corporate bond market that still doesn’t trade electronically today.

“The other thing that happens when you launch something new is everybody says, ‘Well, I would never do all my business that way.’ But the reality is, I’m not trying to do all your business that way,” he says. “I’m very happy with 1–2% because I know 1–2% will lead to 2-4%, which will then lead to 5-7%. It happens incrementally.”

That’s what happened for Toffey at Tradeweb, but didn’t happen at Benchmark Solutions. Soon enough, LTX may find itself in the position of tie-breaker.

Further reading

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@waterstechnology.com or view our subscription options here: http://subscriptions.waterstechnology.com/subscribe

You are currently unable to print this content. Please contact info@waterstechnology.com to find out more.

You are currently unable to copy this content. Please contact info@waterstechnology.com to find out more.

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@waterstechnology.com

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@waterstechnology.com

More on Data Management

New working group to create open framework for managing rising market data costs

Substantive Research is putting together a working group of market data-consuming firms with the aim of crafting quantitative metrics for market data cost avoidance.

Off-channel messaging (and regulators) still a massive headache for banks

Waters Wrap: Anthony wonders why US regulators are waging a war using fines, while European regulators have chosen a less draconian path.

Back to basics: Data management woes continue for the buy side

Data management platform Fencore helps investment managers resolve symptoms of not having a central data layer.

‘Feature, not a bug’: Bloomberg makes the case for Figi

Bloomberg created the Figi identifier, but ceded all its rights to the Object Management Group 10 years ago. Here, Bloomberg’s Richard Robinson and Steve Meizanis write to dispel what they believe to be misconceptions about Figi and the FDTA.

SS&C builds data mesh to unite acquired platforms

The vendor is using GenAI and APIs as part of the ongoing project.

Aussie asset managers struggle to meet ‘bank-like’ collateral, margin obligations

New margin and collateral requirements imposed by UMR and its regulator, Apra, are forcing buy-side firms to find tools to help.

Where have all the exchange platform providers gone?

The IMD Wrap: Running an exchange is a profitable business. The margins on market data sales alone can be staggering. And since every exchange needs a reliable and efficient exchange technology stack, Max asks why more vendors aren’t diving into this space.

Reading the bones: Citi, BNY, Morgan Stanley invest in AI, alt data, & private markets

Investment arms at large US banks are taken with emerging technologies such as generative AI, alternative and unstructured data, and private markets as they look to partner with, acquire, and invest in leading startups.