Esma: Firms struggled with trade data porting after CME wind-down

The EU regulator had to coordinate efforts with local NCAs to clamp down on failures made by counterparties to meet Emir guidelines for porting data.

In May 2020, the Chicago Mercantile Exchange announced plans to wind down several of its regulated businesses, including its European trade repository (TR), CME ETR. The rollback meant that thousands of regulated market participants reporting trade data to ETR would have six months to reroute their reporting flows to a new TR ahead of November 30, 2020, when the services were scheduled to be terminated. However, in a report published on April 15, European regulator the European Securities and Markets Authority (Esma) said that some counterparties failed to follow Esma’s guidelines on porting data from one TR to another.

“The process that the TRs and the counterparties should follow is described in the guidelines on portability,” said Jakub Brettl, senior supervision officer at Esma, during a press briefing on April 28, in response to questions from WatersTechnology. “It’s really important that this process is followed, because that way we can ensure that there is, indeed, no impact on data quality and data integrity [on reporting data].”

Esma’s guidelines for porting were finalized in 2017, and aim to make it easier for reporting entities to move records from one TR to another so they can easily change providers if they want to, and to establish a consistent way of doing so. Reporting entities must move all their open and historical trade data to their new TR so regulators in each jurisdiction can access the reports.

The guidelines also say that the new TR should not accept duplicate reports by TR participants, and the old TR should not accept reports with action types “cancelation” or “error” made by TR participants.

However, Brettl said, some counterparties that were customers of CME ETR failed to port their historical data to their newly designated TR. Instead, they sent cancelation messages on their existing derivatives records with CME ETR, intending to start afresh when reporting to their new TR.

If reporting parties do not follow Esma’s porting guidance, Brettl said, it can distort reported data flows, hampering the regulator’s ability to monitor the market.

“This causes, of course, many problems, because if historical data stays in the old TR, it creates certain spurious, fake data flow, if you will, because these cancellations do not represent real economic activity, which is what we want to capture. So, it creates a certain level of noise,” he said.

During the CME porting window, Esma told local regulators (National Competent Authorities, or NCAs) and the EU TRs to be on the lookout for porting that did not follow its guidelines.

“We have been very clear to the TRs, and we’ve tried to be clear to everyone, that this is not the way to do reporting. Whenever we saw, with the assistance of the TRs, that there might be clients attempting such ways of moving the data, we communicated with the NCAs to get them involved,” Brettl said.

A spokesperson for CME says ETR noticed some isolated cases where clients transferred data using a procedure that did not follow Esma’s guidance. They said that after an investigation, CME stressed the importance to its customers of following the porting procedures during the transfer period.

Brettl said during the briefing that while the porting activities surrounding CME’s exit last summer could be described as an “intensive process,” Esma didn’t observe “unacceptable or significant data quality issues” relating to counterparties’ reporting data.

Esma’s April 15 report examined the quality of the data submitted to TRs under the European Markets Infrastructure Regulation (Emir) and the Securities Financing Transaction Regulation (SFTR). The report says that—in addition to CME’s commercial decision to shut ETR—Brexit also triggered changes in TR market structure that led to a high volume of data being ported in Q4.

Other factors contributing to higher than normal activity over the same period included Intercontinental Exchange’s decision last year to wind down its own Trade Vault rather than provide TR services in the EU post-Brexit (though this wind-down was on a smaller scale than CME’s ETR business), and the creation of other new TRs to support reporting, post-Brexit. For example, the Depository Trust and Clearing Corporation and the London Stock Exchange’s UnaVista established TRs in the EU, and Regis-TR established a UK TR—all of which involved shifting records from their UK to their EU TRs. There are now four TRs offering services in the EU for both Emir and SFTR—the DTCC’s DDRIE, UnaVista, Regis-TR, and KDPW.

Complex operation

John Kernan, CEO of Regis-TR UK, says that all counterparties that moved data from CME ETR to Regis-TR during the transfer window ported all their open and historical trades. However, he says, there were some teething problems in porting data in the format used by CME to that of Regis-TR or processing old reporting data that predated revisions made in 2017 to reporting practices under Emir. Under these updated regulatory technical standards (RTS), counterparties had to follow set standards for reporting to a new TR, ensuring, for example, that both parties to a trade agreed that the reported data was correct.

“One would assume that because it is in the RTS that it [the reported data] should be easily portable, and I guess that’s broadly true, but you also need to remember that just because it’s in RTS quality [follows the regulatory technical standards under Emir] it doesn’t necessarily mean that it just lifts and drops perfectly from one TR to the other,” Kernan says.

Also, TRs use their own proprietary formats for reporting data, Kernan says, which complicates porting. This is expected to change under updates to Emir, known as “Emir Refit,” which harmonizes reporting standards by forcing TRs and counterparties to report using machine-readable XML schemas.

But TR schemas are not the only challenge when porting data, Kernan adds: historical data that predates the 2017 RTS standards is also difficult to migrate.

“TRs were having to put in historical data that was not in the RTS quality. For example, it could be in CSV (comma-separated variable) format,” he says.

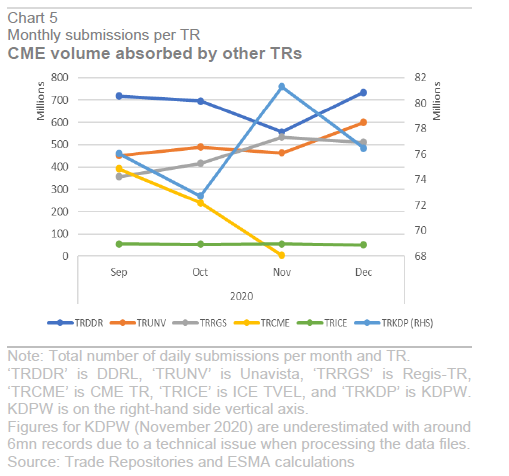

The report says that from about 400 million submissions to CME’s ETR in the month of September 2020, its volume sharply reduced. UnaVista and Regis-TR were two of the biggest recipients of reporting flow from the CME ETR unwind, with an increase of more than 150 million submissions between September and December 2020.

Brettl said that this was a complex operation given the volumes of the transactions and the relatively brief window of time to complete switchovers.

“You can imagine that, particularly during the peak months of this porting from CME to other TRs, there were large amounts of data and many clients being moved, mainly during the weekends,” Brettl said.

In some instances, counterparties were slow to select new providers during the transfer window and had to be prompted by the regulators to act quicker, Brettl said.

“It’s not something that can be typically performed on one day’s notice, and so those cases, those counterparties that we observed that were a bit slow in selecting a new TR we had been actively engaging with the NCAs to then make sure that they, on their side, can engage with those counterparties and make sure that everything goes well,” Brettl said.

Towards the end of the transfer period, Regis-TR’s Kernan says that Esma selected several counterparties that had large sums of non-RTS quality data and allocated them with a new TR. Under Esma guidelines, the regulator can appoint a TR, if an old TR has not notified Esma about a new TR or if the new TR refuses to receive the counterparties’ data.

“Esma took that list of clients and allocated them out to the TRs, so there wasn’t a selection process or anything like that on our part. Towards the end of the CME wind-down, each TR received a number of clients with old historical data that wasn’t the requisite standard,” he says.

It took some counterparties nine months to port their data to a new TR, Brettl said during the press briefing. While the May-to-November transfer window given to counterparties was six months, and not nine, Esma was notified of the unwinding prior to the public announcement, says an Esma spokesperson, responding by email to WatersTechnology.

“Esma knew about the wind-down plans well in advance and we had been discussing operational aspects with the TR well ahead of the public announcement. CME’s operations ceased in November, but technically speaking the wind-down was formalized by the withdrawal of the registration by Esma in December,” the spokesperson says.

The official deadline for the wind-down was deemed December 2020, they say, and that all open and historical data was successfully ported to other TRs ahead of Brexit.

A spokesperson for CME says that once all clients were successfully offboarded and their “live” data ported—which was completed by November 30—there was a further few weeks of porting of historical (that is, non-“live”) data from the CME ETR to other TRs. WatersTechnology understands that while the client-facing porting process took six-and-a-half months, the overall timeline for the CME TR wind-down from start to finish was closer to eight to nine months.

UnaVista and the DTCC declined to comment for this article.

Only users who have a paid subscription or are part of a corporate subscription are able to print or copy content.

To access these options, along with all other subscription benefits, please contact info@waterstechnology.com or view our subscription options here: http://subscriptions.waterstechnology.com/subscribe

You are currently unable to print this content. Please contact info@waterstechnology.com to find out more.

You are currently unable to copy this content. Please contact info@waterstechnology.com to find out more.

Copyright Infopro Digital Limited. All rights reserved.

As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (point 2.4), printing is limited to a single copy.

If you would like to purchase additional rights please email info@waterstechnology.com

Copyright Infopro Digital Limited. All rights reserved.

You may share this content using our article tools. As outlined in our terms and conditions, https://www.infopro-digital.com/terms-and-conditions/subscriptions/ (clause 2.4), an Authorised User may only make one copy of the materials for their own personal use. You must also comply with the restrictions in clause 2.5.

If you would like to purchase additional rights please email info@waterstechnology.com

More on Regulation

Off-channel messaging (and regulators) still a massive headache for banks

Waters Wrap: Anthony wonders why US regulators are waging a war using fines, while European regulators have chosen a less draconian path.

Banks fret over vendor contracts as Dora deadline looms

Thousands of vendor contracts will need repapering to comply with EU’s new digital resilience rules

Chevron’s absence leaves questions for elusive AI regulation in US

The US Supreme Court’s decision to overturn the Chevron deference presents unique considerations for potential AI rules.

Aussie asset managers struggle to meet ‘bank-like’ collateral, margin obligations

New margin and collateral requirements imposed by UMR and its regulator, Apra, are forcing buy-side firms to find tools to help.

The costly sanctions risks hiding in your supply chain

In an age of geopolitical instability and rising fines, financial firms need to dig deep into the securities they invest in and the issuing company’s network of suppliers and associates.

Industry associations say ECB cloud guidelines clash with EU’s Dora

Responses from industry participants on the European Central Bank’s guidelines are expected in the coming weeks.

Regulators recommend Figi over Cusip, Isin for reporting in FDTA proposal

Another contentious battle in the world of identifiers pits the Figi against Cusip and the Isin, with regulators including the Fed, the SEC, and the CFTC so far backing the Figi.

US Supreme Court clips SEC’s wings with recent rulings

The Supreme Court made a host of decisions at the start of July that spell trouble for regulators—including the SEC.